Is Taiwan Semi conductors a buy in 2023/2024?

Taiwan Semiconductor Manufacturing Company (TSMC) is the world’s leading foundry with a ~60% market share of the global semiconductor foundry segment, representing ~30% of the world semiconductor output value in 2022 (excluding memory). The company has a near-monopoly in the most advanced node sizes, with a ~90% market share.

The company has a market cap of $501 billion, has generated $75 billion of revenue in the last twelve months, and its balance sheet has $23 billion in net cash.

Financial highlights (these are all on a TTM basis as of Q1 2023):

Revenue CAGR of 15.9% since 2009 and 15.6% over the last 10 years

FCF / share CAGR of 9.6% since 2009 and 35.3% over the last 10 years

Net income / share CAGR of 20.6% since 2009 and 19.5% over the last 10 years

Median ROE of 24% since 2009 and over the last 10 years

Median P/E since 2009 from 14-16x and from 16-18x over the last 10 years

Currently trades for 15.1x TTM EPS (stock is at 593 TWD)

6.6% earnings yield, 3.3% FCF yield

On enterprise value, a 7.0% earnings yield, 3.5% FCF yield

The drivers of TSMC’s revenues are how many wafers its fabs can ship per year, and what price TSMC gets on those wafers. Quality and throughput matter, and TSMC is the best at both. The company has a demonstrated ability to remain competitive at ever-smaller node processes, which are more complex and difficult to fabricate.

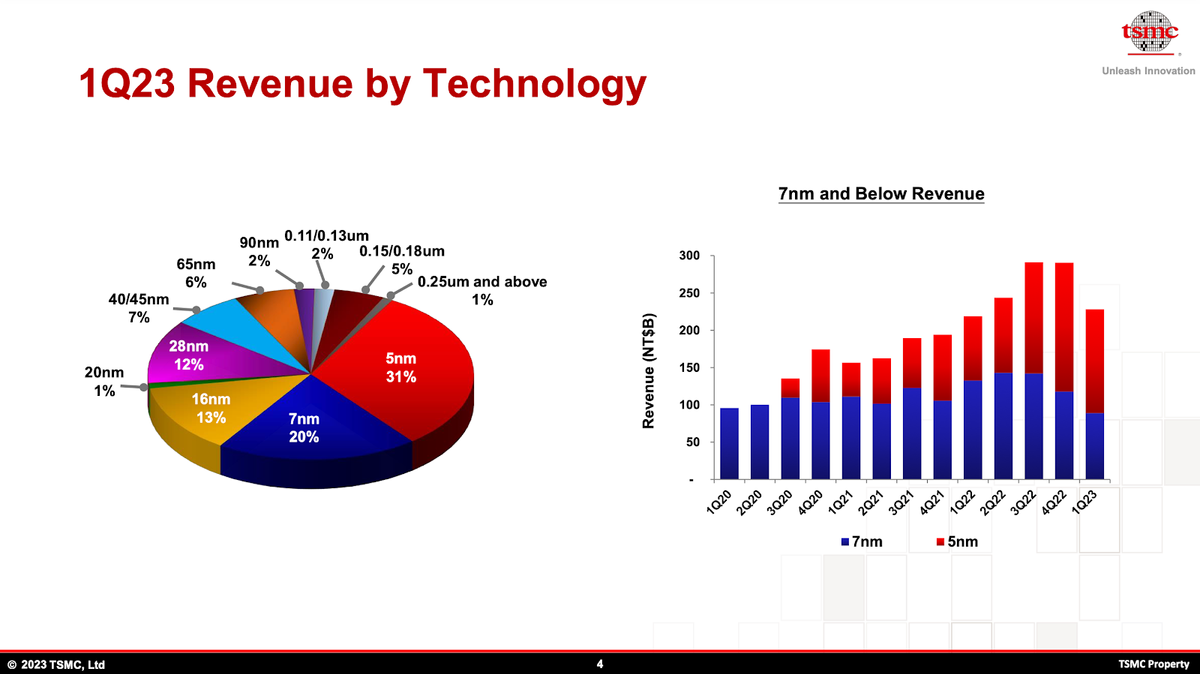

Over the last 9 years, wafer throughput at TSMC has grown at 9.2% CAGR and revenue has grown at 16% CAGR (in TWD), demonstrating rising wafer ASP as TSMC has shifted revenue to smaller node sizes.

For example, 10 years ago this is what TSMC’s revenue by technology looked like:

And this is what it looks like now:

During that time revenue grew from NT$ 0.5 billion to NT$ 2.3 billion.

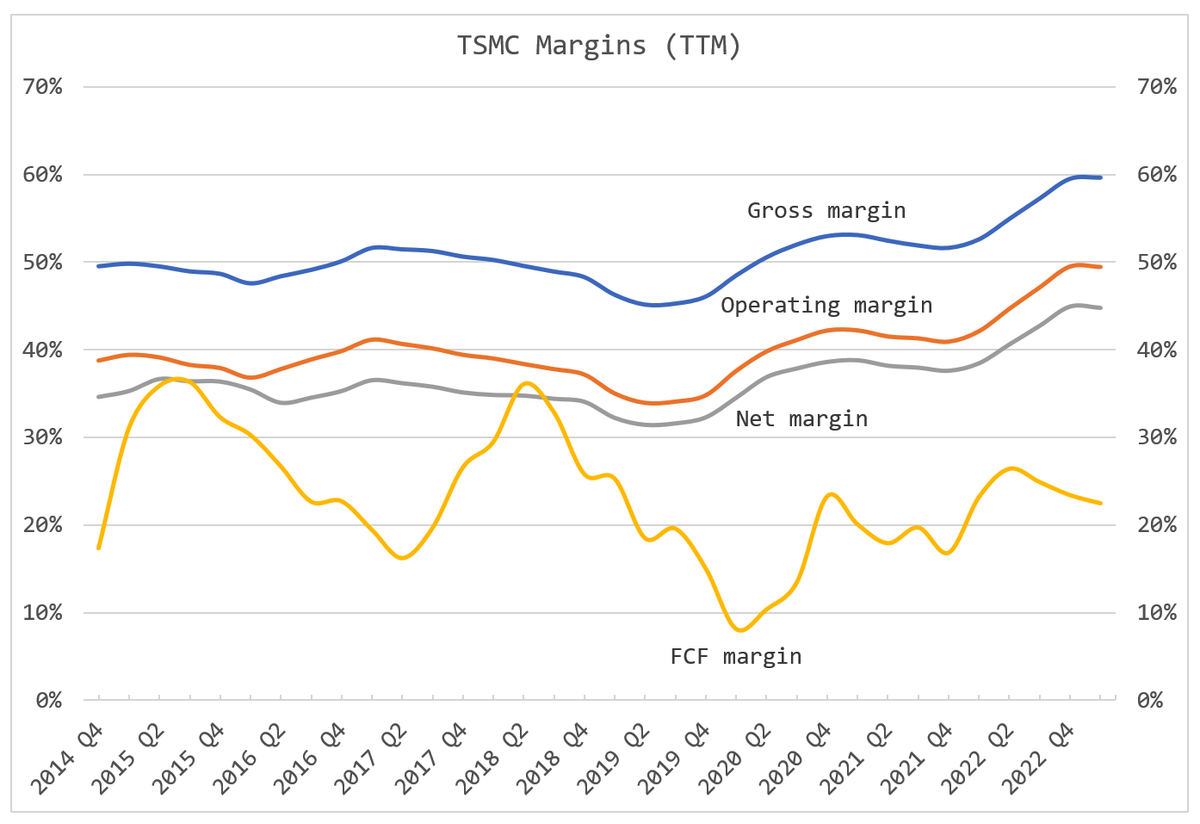

We can observe this rising ASP and benefits of specialization in TSMC’s margins over the years:

TSMC is the best and most trusted operator of semiconductor fabs.

This is TSMC’s vision:

TSMC has been able to deliver on its vision, as evidenced by its leading market share.

Over the years, as nodes have shrunk, so has the competition. At smaller node sizes, TSMC has an overwhelming competitive position, with Samsung as a small 2nd place. “The cowards never started, and the weak died along the way.”

It is not far-fetched to say that TSMC has a near monopoly in advanced nodes:

Business Merits

TSMC was founded in 1987 by Morris Chang, a Chinese native who studied at Harvard, MIT and Stanford, and subsequently went to work for Texas Instruments for 25 years.

Chang increasingly saw the need for outsourced semiconductor fabrication services, so he moved to Taiwan and started TSMC.

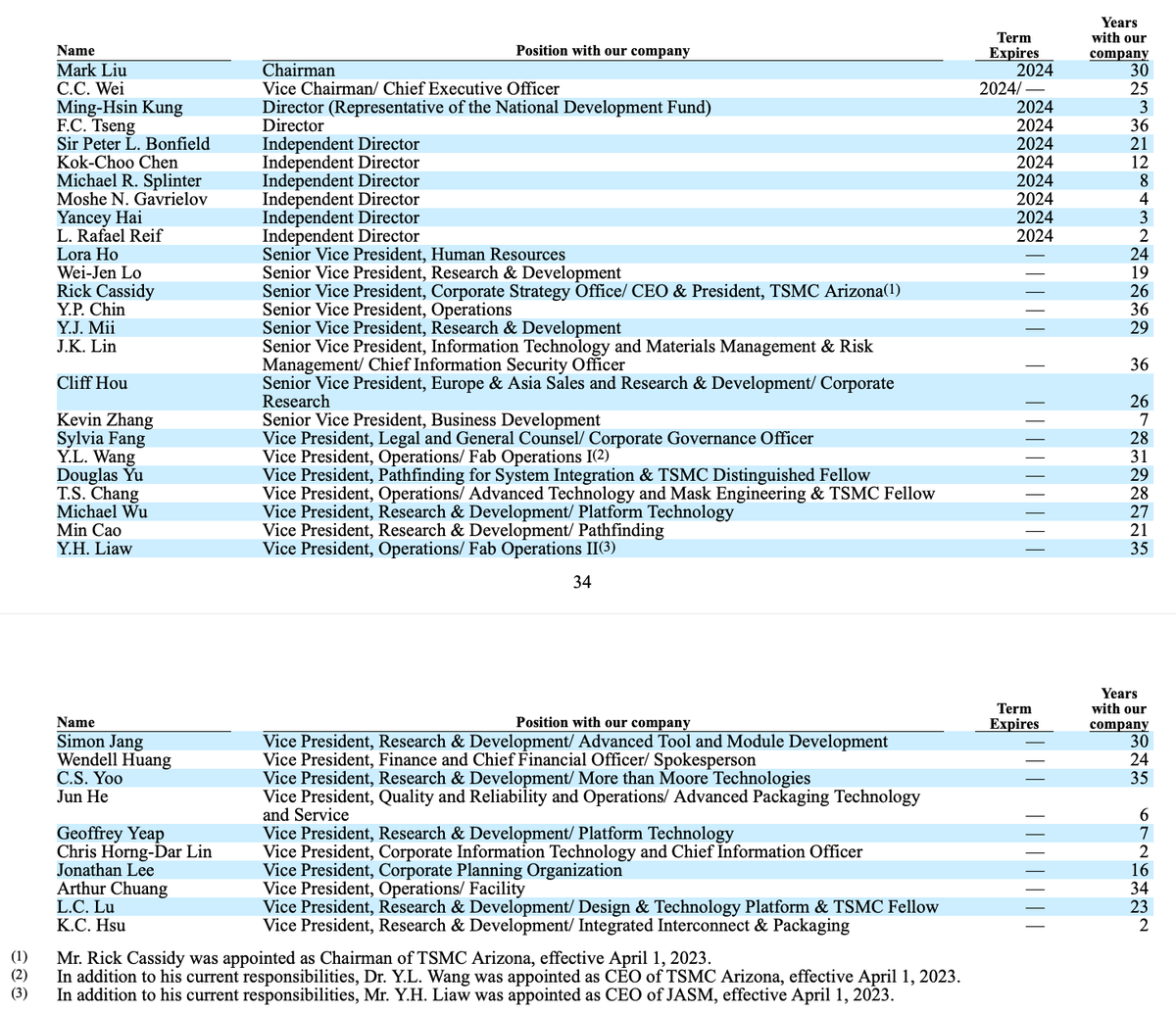

Chang is currently 91 years old and no longer at the company, however current executives have a very long tenure and are very well regarded:

TSMC has made possible the rise of the fabless semiconductor manufacturer, like Nvidia and AMD. And, of course, it has allowed Apple to move away from Intel by designing its own silicon. Apple is believed to be about one quarter of TSMC’s revenues: https://focustaiwan.tw/business/202303030016

While TSMC has hundreds of customers, its ten largest customers accounted for 68% of total revenues in 2022.

Here is a good article on the rise of TSMC:

https://www.ft.com/content/05206915-fd73-4a3a-92a5-6760ce965bd9

TSMC does not compete with its customers; it does not build any proprietary chips. It instead works closely with its customers and suppliers and orchestrates billions of dollars worth of machines in order to achieve the precise process, throughput, and cost needed. In 2022 “we deployed 288 distinct process technologies, and manufactured 12,698 products for 532 customers.”

Samsung is Apple's smartphone rival, so it's unlikely that Apple would like to expand its relationship with them (in 2011, Apple sued Samsung for stealing some of its designs).

The long-term trends for TSMC remain positive. Semiconductors are a cyclical industry that grows over time as evidenced by the volume and revenue CAGR numbers shared above.

Below are the tables used to generate those numbers. There are streaks of negative YoY revenue growth in some periods but overall, this is a secular growth industry:

Smaller nodes (measured in nanometers) are required to pack more transistors on a wafer. Transistors are on/off switches and are used by software for computation. The more transistors, the more computation per area. This has allowed chips to become faster and more power efficient. It’s the reason everyone can have a supercomputer in his pocket with an iPhone, for instance.

At the same time, older nodes (larger nanometer sizes) continue to be popular for industrial and automotive use cases. Thus, TSMC keeps adding fab capacity mostly for leading edge nodes, but keeps on chugging along with older nodes as well.

In addition to the secular growth trends, there is now an onshoring trend. Countries around the world are trying to get TSMC to build fabs so that they can evade China-related risks (see below in the Risks section).

TSMC management has repeatedly noted that it costs anywhere from 2x-5x to build fabs outside of Taiwan. Running a fab also requires around the clock work by dedicated employees, and TSMC executives have noted that the work ethic of Americans is not up to par. This is why today most of TSMC’s fabs are in Taiwan.

From the 20-F:

We currently operate one 150mm wafer fab, six 200mm wafer fabs, five 300mm wafer fabs, and five advanced backend fabs. Our corporate headquarters and eight of our fabs are located in the Hsinchu Science Park, two fabs are located in the Central Taiwan Science Park, four fabs are located in the Southern Taiwan Science Park, one fab is located in the United States, one fab is located in Shanghai, and one fab is located in Nanjing.

https://www.tsmc.com/english/aboutTSMC/TSMC_Fabs

However, with government incentives and political pressure, TSMC is now building advanced fabs in Arizona and Japan. Other countries might follow.

The cost of fabs has risen exponentially over the years. It used to cost less than $1 billion to build a fab; today it costs $20 billion and even more, depending on the fab’s capacity. This “price of admission” is an additional barrier to entry. Even if a competitor such as Intel were to throw this much money at the problem, they do not have the know-how to operate a leading fab at adequate yields, something that TSMC has learned over decades.

TSMC’s leadership and enduring success is the result of its strong culture. It is likely, therefore, that TSMC can maintain and extend its leadership position over time.

Risks

TSMC’s fabs are mostly in Taiwan. For all intents and purposes—when considering the most advanced nodes—they are all in Taiwan.

China will eventually take over Taiwan. As one observer has noted, it is not necessary to read between the lines, one only has to read the lines. Xi Jinping has been talking about this for a long time. It is a Chinese objective to take over Taiwan, by force if need be.

Taiwan is obviously well aware of this. A Taiwan admiral said: "It is not a matter of if they will invade. It's a matter of when they will invade."

The 60 Minutes segment on Taiwan is worth watching: https://youtu.be/akCU6wSLAR4

A lot has been written on this topic and of course it has been war-gamed to death:

It has been said that Taiwan’s best defense is a porcupine strategy, i.e., to make itself hard to invade.

There are two views overall on this. One view is to avoid TSMC as an investment altogether. This is probably what led Buffett to sell most of his TSMC stake.

The other view goes something like this: “If China invades Taiwan, there will likely be a war similar to Ukraine’s, with broad international support on Taiwan’s behalf. Since TSMC is 30% of global semiconductor output and 90% of all advanced output, the world economy will grind to a halt. So what’s the point in avoiding an investment in TSMC?”

Personally, I fall somewhere in between: I invest in TSMC, but keep it at a small percentage of NAV. Caveat Emptor.

There is also competition risk. Intel is trying to become a leading-node fab. I will believe it when I see it. It is very hard to be a leading-node fab. All of TSMC’s competitors have given up, with the exception of Samsung.

Finally, there is customer concentration risk. Apple is about a quarter of TSMC’s sales. In total, North America accounted for 68% of TSMC’s revenues last year. By sales, this is an American company. It’s in America’s (and the world’s) interest to defend it.

Pre-Mortem: Why did this investment fail?

Poor management would sink this company. In order to function, it needs excellent management. I don't think this is a "ham sandwich business."

The biggest failure however would be if the CCP takes over TSMC and deprives the world of leading node chips. But then, as they say, we'll have bigger problems.